Intro: The monetary policy of India is a vital aspect of the country's economic framework, playing a pivotal role in regulating the supply of money and credit in the economy. The Reserve Bank of India (RBI) serves as the central monetary authority and is responsible for formulating and implementing the monetary policy. The primary objective of the monetary policy is to maintain price stability while also considering the goal of fostering economic growth. The monetary policy framework in India has evolved significantly over the years (Rao, 2014). In 2016, the RBI Act was amended to establish a statutory and institutionalized framework for a Monetary Policy Committee (MPC) to ensure the maintenance of price stability. The MPC is entrusted with the task of fixing the benchmark policy rate, known as the repo rate, which is the rate at which the central bank lends to commercial banks. The current repo rate in India is 6.5%.

In addition to the repo rate, the RBI uses a range of other instruments to conduct monetary policy, including the reverse repo rate, the cash reserve ratio (CRR), the statutory liquidity ratio (SLR), and the marginal standing facility (MSF). These instruments are employed to regulate the availability of credit and money supply in the economy. For instance, the CRR is the percentage of a bank's total deposit that it must maintain as reserves with the central bank, while the SLR is the share of net demand and time liabilities that banks are required to maintain in safe and liquid assets such as government securities, gold, and cash The RBI's monetary policy is also guided by an inflation targeting framework. The central bank, in consultation with the government, has set an inflation target of 4% with a tolerance band of ±2% for the period 2016-2021. This framework aims to ensure that inflation remains within a specified range, thereby contributing to macroeconomic stability and sustainable economic growth (Glenn, 2018).

The RBI's monetary policy department plays a crucial role in providing the necessary support for the MPC in formulating the monetary policy (Mark, 2015).

Fig 1.1 Monetary Policies of RBI

Source. Fintra

1.1 Banking System in India

The banking system in India is a critical component of the country's financial infrastructure, encompassing a diverse array of institutions and playing a central role in the nation's economic development. The Indian banking sector is broadly classified into scheduled banks and non-scheduled banks. Scheduled banks are those included in the Second Schedule to the Reserve Bank of India, and they are further categorized into commercial banks and cooperative banks. On the other hand, non-scheduled banks are those that are not included in the Second Schedule (Sudha,2019).The Indian banking system comprises various categories of banks, including public sector commercial banks, private sector commercial banks (including both domestic and foreign banks), regional rural banks, cooperative banks, small finance banks, and payment banks. Public sector banks, such as the State Bank of India and its associates, have historically dominated the banking industry in India. However, private and foreign banks have also made significant inroads, capturing a growing market share in terms of deposits and advances.

1.2 Monetary policy and the relation with banks

Monetary policy, as a critical instrument of economic management wielded by central banks, plays a pivotal role in shaping the financial landscape of a nation. Its impact reverberates through various sectors, with the banking industry standing as a key arena where the consequences are keenly felt. The intricate relationship between monetary policy and banking operations is marked by a constant interplay of forces, influencing not only the profitability but also the liquidity dynamics of financial institutions. The early proponents of contemporary economics have long been researching the direct relationship between bank profitability and monetary policy. A straightforward maturity mismatch can have an impact on bank profitability and margins. If the average duration of the financial system's inflows surpasses that of its outflows, an increase in interest rates is detrimental to it (Alexander, 2021). Throughout economic history, the symbiotic connection between monetary policy and banks has been evident. Central banks, armed with tools such as interest rates, reserve requirements, and open market operations, actively shape the cost and availability of money within the economy. These policy decisions, in turn, propel a cascade of effects that permeate the intricate workings of banks, shaping their lending practices, investment strategies, and overall financialhealth. The banking industry is essential to the flow of capital required for the corporate sector to operate smoothly, improving the chances of a stronger economy. In a same vein, the RBI effectively manages the money supply through the quantitative tools of monetary policy. To actively control the banking system, the following monetary policy measures are used: Bank Rate (BR), Cash Reserve Ratio (CRR), Statutory Liquidity Ratio (SLR), Repo Rate (RR), Reverse Repo Rate (RRR), and Marginal Standing Facility (MSF) (Meraj, 2019).

This research embarks on a journey to unravel the nuanced ways in which the policies crafted by the Reserve Bank of India (RBI) resonate within banks, focusing particularly on the divergence between public and private sector entities. As we navigate through the empirical landscape of this study, it becomes imperative to recognize that monetary policy serves as a compass guiding banks through economic currents. Whether through adjustments in interest rates to spur economic activity or changes in reserve requirements to ensure financial stability, every policy move leaves an indelible mark on the strategies and performance metrics of banks. The amount of money created on the one hand and the amount of money that is demanded by the economy on the other are used to gauge the profitability of banks (Meraj, 2019).

Against this backdrop, this research seeks to delve deeper into the impact of monetary policy on two crucial dimensions of bank functioning: profitability and liquidity. By scrutinizing selected private sector behemoths - HDFC, ICICI, and Kotak Mahindra - alongside prominent public sector stalwarts - PNB, SBI, BOB, we aim to offer a comprehensive analysis that illuminates the divergent paths these banks tread in response to the ebbs and flows of monetary policy. In essence, this research endeavors to contribute to the broader discourse on monetary policy effectiveness by shedding light on its intricate dance with the banking sector in India.

1.3 Objectives of Study- The following are the objectives of the paper-

To analyze the impact of changes in monetary policy on the profitability of public and private sector banks in India over a specific period.

To assess the influence of monetary policy on the liquidity positions of public and private sector banks in India, considering different phases of the monetary policy cycle.

To compare the responses of public and private sector banks in India to changes in monetary policy and evaluate the variations in their profitability and liquidity metrics.

1.4. Limitations of Study

The findings of this study may not be fully generalizable to all public and private sector banks in India. The selection of a specific sample of banks for analysis may not accurately represent the entire banking sector, leading to potential limitations in the applicability of the study's findings. The unique characteristics, market conditions, and regulatory environments of banks not included in the study may result in different outcomes, highlighting the need for caution when extrapolating results to the broader banking landscape. The study relies on secondary data obtained from financial reports and other sources, which may introduce limitations in terms of accuracy, completeness, and availability. While efforts have been made to ensure the reliability of the data, reliance on historical information may constrain the analysis to certain periods, potentially overlooking recent developments or changes in banking practices. It's important to acknowledge these constraints and their potential impact on the robustness of the study's findings.

2. Literature Review

Hancock (2023) provides a comprehensive analysis of the relationship between bank profits, interest rates, and various components of monetary and regulatory policy and the findings indicate that bank profits are more responsive to changes in loan rates than deposit rates, and increases in interest rates, while keeping the spread unchanged, lead to higher variable pLrofits, supporting the hypothesis that banks benefit from high interest rates. The paper concludes by discussing the policy implications of its findings, particularly in evaluating the impact of expanding reserve requirements on other financial firms. M. Sumathy and Jisha T. P.(2022) investigates the impact of monetary policy instruments on the profitability of the State Bank of India (SBI), the largest public sector bank in India, over the period from 2018 to 2021 and the findings indicate a significant influence of monetary policy instruments on the profitability of SBI, advocating for careful consideration by the central bank in formulating policies aligned with prevailing economic conditions to prevent disruptions in the money supply within the market. Alexander et al. (2021) summarize their findings, indicating several significant relationships. Firstly, they identify a positive long-run association between Liquidity Ratio and bank profitability, suggesting that higher liquidity levels within banks contribute to enhanced profitability over time. Secondly, the study reveals a negative long-run relationship between Interest Rate and bank profitability, implying that higher interest rates may adversely impact the profitability of banks in the long term. Finally, the research highlights a positive long-run relationship between Money Supply (M2) and bank profitability, indicating that an increase in money supply tends to bolster bank profitability over the long haul. Kumar et al. (2020) delves into the intricate relationship between monetary policy and bank profitability in New Zealand, utilizing the generalized method of moments (GMM) estimator. The results reveal that an escalation in short-term interest rates corresponds with an augmentation in bank profitability, contrasting with the adverse effect observed with an increase in long-term interest rates, which tends to diminish bank profitability. Moreover, the analysis extends beyond monetary policy indicators, shedding light on additional determinants influencing bank profitability within the New Zealand context.

Meraj Banu and Sudha Vepa (2019) analyze the impact of monetary policy instruments on the revenue and profitability of the State Bank of India (SBI), the largest public bank in India. The findings suggest a positive relationship between the monetary policy variables and the operational performance of SBI. However, none of the variables directly influence the net profit of the bank. The paper concludes that factors other than monetary policy variables, such as adjustments of provisions and contingencies, may influence net profitability.

Kaspar Zimmermann (2019) explores the relationship between monetary policy and bank profitability using a newly compiled dataset covering 17 countries over a period of 145 years. The paper contributes to the understanding of the complexities surrounding monetary policy and its implications for bank profitability, providing valuable insights for policymakers and researchers alike. Diana (2019) study delves into the crucial question of how historically low monetary policy interest rates, spurred by expansionary monetary policies post the 2007/2008 financial crisis, impact bank profitability in developed economies. The study, which focuses on European and Japanese banks during the post-crisis period from 2010 to 2018, aims to explore the relationship between decreases in monetary policy rates and bank profitability, investigating whether this correlation is linear and how it influences banks' ability to lend and the transmission of monetary policy. The findings reveal a nuanced relationship between monetary policy rates and bank profitability: initially, as monetary policy rates decrease, bank profitability tends to increase, but only up to a certain low threshold. Beyond this threshold, however, the relationship becomes inverted, with both variables increasing simultaneously. Carlo et al. (2018) delve into the impact of both standard and non-standard monetary policies on bank profitability. The findings of the study reveal several key insights and suggest that while accommodative monetary conditions may initially impact bank profitability negatively, other factors come into play to mitigate this effect. Rudebusch (2018) examines the Federal Reserve's adoption of unconventional monetary policy tools in response to the constraints imposed by near-zero short-term interest rates over the past decade. The paper provides a concise overview of the challenges faced by the Federal Reserve in the aftermath of the global financial crisis and the Great Recession. It underscores the limitations posed by the zero lower bound on short- term interest rates and the subsequent necessity for unconventional policy interventions. Rudebusch's analysis is focused on evaluating the efficacy of two specific unconventional monetary policy tools employed by the Fed: forward guidance and quantitative easing. Forward guidance involves the central bank communicating its future policy intentions to influence market expectations and guide economic decisions. Rakesh Mohan and Partha Ray (2018) highlighted the dominance of joint monetary and fiscal stimuli by Indian authorities in the period 2009-13, in response to the NAFC, which possibly contributed to rising inflation and external account instability. The paper evaluates how monetary policy has grappled with managing the "impossible trinity" in these contexts, navigating between exchange rate stability, monetary autonomy, and capital mobility. Overall, the paper provides valuable insights into the evolution of Indian monetary policy amidst economic challenges and policy reforms, offering a nuanced analysis of its effectiveness and resilience in addressing inflation-targeting objectives and managing significant macroeconomic events. Kaspar Zimmermann (2017) examines the impact of monetary policy on the banking sector from a long-term perspective and the findings indicates that changes in policy rates have a significant impact on the profitability of deposit-taking activities within banks. Moreover, the abstract suggests that, on average, bank profitability tends to decline following a policy rate hike. Sergius (2015) raises four research questions and formulates corresponding hypotheses to guide the analysis. The findings of the study reveal that while certain monetary policy instruments, such as the minimum rediscount rate, have a significant impact on Zenith Bank Plc's profitability, others such as cash reserve ratio, liquidity ratio, and interest rate do not exhibit significant effects. This highlights the complexity of the relationship between monetary policy and bank profitability, suggesting that the effectiveness of monetary policy instruments may vary depending on the specific context and economic conditions. Lia Amaliawiati and Edi Winarso (2015) investigate the influence of the Bank Indonesia Rate (BI Rate), a key monetary policy tool in Indonesia, on the profitability of conventional commercial banks listed on the Indonesia Stock Exchange. And the analysis reveals that while the BI Rate significantly influences ROA, other factors such as Operational Cost to Operational Income (OCTOI) exert substantial influence on NIM. Overall, this research contributes to understanding the intricate relationship between monetary policy, represented by the BI Rate, and bank profitability in the Indonesian context, offering insights that are crucial for policymakers and banking sector stakeholders alike. Leena Kaushal and Neha Pathak (2013) delves into the intricate relationship between monetary policy changes, inflation, and banking sector profitability in India, Through their analysis, the authors reveal a significant impact of policy changes on both commercial banks' interest profitability and inflation levels. Importantly, the study highlights the adaptability of commercial banks in response to shifts in monetary policy stances, particularly when policies tighten.

3. Research Methodology

The methodology involves a comprehensive analysis and comparison of selected banks, including HDFC, ICICI, Kotak Mahindra, PNB, SBI, and BOB, utilizing regression, correlation, and descriptive statistics. By focusing on key indicators such as net interest margin and Casa Ratio, the research seeks to unravel the intricate relationships between monetary policy instruments and bank performance metrics, providing valuable insights into the transmission mechanisms of monetary policy in the banking sector. Many existing studies overlook the unique characteristics and responses of public and private sector banks to monetary policy changes, treating them as homogeneous entities. Another gap in the literature is the lack of studies utilizing the latest available data to assess the impact of monetary policy on bank performance. The research addresses this by incorporating the most recent data available, ensuring that the analysis reflects current market conditions and policy dynamics. The Independent Variable taken for this study are repo rate. reverse Repo CRR and SLR and the dependent Variables are the CASA Ratio and Net Interest Margin (NIM). The sampling size for this study encompasses data from the previous 10 years (2013- 2022), with yearly observations collected for each selected bank. Several data sources were utilized to obtain the necessary information, ensuring the reliability and validity of the dataset. Cash Reserve Ratio data was sourced from the Reserve Bank of India (RBI) publications, including monetary policy reports and statistical bulletins. Similar to the CRR, SLR data was obtained from RBI publications, Repo Rate and Reverse Repo Rate were sourced from RBI publications. The study applied statistical tools like regression, correlation, unit root test and granger causality test etc. to examine the association between dependent and independent variables. Based on the previous literature the following hypothesis has been framed.

Hypothesis 1-

H0- Changes in monetary policy do not significantly impact the profitability of both public and private sector banks in India.

H1- Changes in monetary policy significantly impact the profitability of both public and private sector banks in India.

Hypothesis 2-

H0- Monetary policy does not significantly influence the liquidity positions of public and private sector banks in India across different phases of the monetary policy cycle.

H1- Monetary policy significantly influences the liquidity positions of public and private sector banks in India across different phases of the monetary policy cycle.

Hypothesis 3-

H0- There are no significant differences in the responses of public and private sector banks in India to changes in monetary policy, resulting in similar profitability and liquidity metrics.

H1- There are significant differences in the responses of public and private sector banks in India to changes in monetary policy, resulting in variations in profitability and liquidity metrics.

The regression equation takes the form: Y=ß0+ß1X1+ß2X2+...+ßnXn+?

Where,

Y represents the dependent variable (profitability or liquidity).

X1, X2,...,Xn are the independent variables (monetary policy variables). X1 = Repo rate

X2 = Reverse Repo Rate X3 = Cash Reserve Ratio

X4 = Statutory Liquidity Ratio

ß0, ß1, ß2,...,ßn are the coefficients representing the relationship between the dependent and independent variables. ? is the error term.

4- Data Analysis and Interpretation –

Table 4.1: Unit Root Test: Public Sector Banks: PP Fisher Chi Square test

| Variables | I (0) | I (1) | Inference |

| Casa Ratio | 8.08 | 18.111* | Stationarity |

| Net Interest Margin | 7.14 | 8.557* | Stationarity |

| Cash Reserve Ratio | 15.687* | 18.905 | Stationarity |

| Statutory Liquidity Ratio | 7.341 | 19.931* | Stationarity |

| Repo Rate | 1.556 | 6.972* | Stationarity |

| Reverse Repo Rate | 1.136 | 4.557* | Stationarity |

Source. EViews

The table presents the results of a unit root test conducted on various variables related to public sector banks. The unit root test, specifically the PP Fisher Chi Square test, is utilized to determine the stationarity of the variables, which is crucial in time series analysis. Upon analyzing various banking indicators, it becomes apparent that each exhibits distinct characteristics regarding their stationarity. The Casa Ratio and Net Interest Margin showcase stationary behavior (I(0)), evidenced by their relatively high values of 8.08 and 7.14, respectively, indicating no further differencing is required for achieving stationarity. Conversely, the Cash Reserve Ratio and Statutory Liquidity Ratio display a different trend, requiring first-order differencing (I(1)) to attain stationarity, with values of 15.687 and 7.341, respectively. This suggests the presence of underlying trends or patterns in the original series that are mitigated through differencing. Similarly, both the Repo Rate and the Reverse Repo Rate exhibit a need for first-order differencing (I(1)) to achieve stationarity, with values of 1.556 and 1.136, respectively.

Table 4.2 Unit Root Test: Private Sector Banks: PP Fisher Chi-Square test

| Variables | I (0) | I (1) | Inference |

| Casa Ratio | 11.148 | 11.703* | Stationarity |

| Net Interest Margin | 1.785 | 12.160* | Stationarity |

| Cash Reserve Ratio | 15.687* | 18.905 | Stationarity |

| Statutory Liquidity Ratio | 7.341 | 19.931* | Stationarity |

| Repo Rate | 1.556 | 6.972* | Stationarity |

| Reverse Repo Rate | 1.136 | 4.557* | Stationarity |

Source. EViews

The unit root test results reveal important insights into the stationarity of various key indicators for private sector banks. The Casa Ratio, representing the proportion of current accounts and savings accounts to total deposits, exhibits stationary behavior at both levels of differencing (I(0) and I(1)), with PP Fisher Chi-Square test statistics of 11.148 and 11.703, respectively, surpassing critical values. Similarly, the Net Interest Margin, a measure of profitability, demonstrates stationarity with test statistics of 1.785 at I(0) and 12.160 at I(1). Additionally, both the Cash Reserve Ratio and the Statutory Liquidity Ratio, regulatory requirements determining liquidity, exhibit stationarity at I(0) and I(1), with test statistics exceeding critical values. Likewise, the Repo Rate and the Reverse Repo Rate, key monetary policy tools, display stationarity at both levels of differencing. Overall, these results indicate that all variables examined for private sector banks maintain stationarity, implying consistent statistical properties over time. Descriptive Statistics.

Table 4.3: Descriptive Statistics: Public Sector Banks

| STATISTIC | CASA RATIO | CRR | NET INTEREST MARGIN | REPO RATE | REVERSE REPO RATE | SLR |

| Mean | 39.59767 | 3.975 | 2.336333 | 6.035 | 5.145 | 20.06 |

| Median | 41.635 | 4.1 | 2.365 | 6.175 | 5.7 | 19.875 |

| Maximum | 46.55 | 4.5 | 2.93 | 8 | 6.25 | 23 |

| Minimum | 25.74 | 3.25 | 1.81 | 4 | 3.45 | 18.15 |

| Std. Dev. | 5.743949 | 0.38344 | 0.294858 | 1.335274 | 1.086306 | 1.69794 |

| Skewness | - 1.217209 | -0.6194 | 0.017089 | - 0.235549 | -0.629255 | 0.31217 |

| Kurtosis | 3.591539 | 2.175783 | 2.350031 | 1.925738 | 1.701627 | 1.72302 |

Source. EViews

The average CASA Ratio for public sector banks is approximately 39.60%, indicating that around 39.60% of their total deposits come from Current Account and Savings Account deposits. The median CASA Ratio is slightly higher than the mean, suggesting a slightly right-skewed distribution. The maximum CASA Ratio observed is 46.55%, indicating that some banks have a relatively high proportion of CASA deposits. The minimum CASA Ratio observed is 25.74%, indicating that some banks have a lower proportion of CASA deposits. The CASA Ratio has a standard deviation of approximately 5.74, suggesting moderate variability around the mean. The CASA Ratio distribution is negatively skewed (- 1.22), indicating that the tail of the distribution is skewed to the left, with more data points on the right side of the mean. The kurtosis value (3.59) suggests that the distribution of CASA Ratio is leptokurtic, meaning it has heavier tails and sharper peaks compared to a normal distribution. CRR distribution is negatively skewed (-0.62), suggesting a slight tail to the left. The kurtosis value (2.18) suggests that the distribution of CRR is platykurtic, meaning it has lighter tails and flatter peaks compared to a normal distribution. The average Net Interest Margin for public sector banks is approximately 2.34%. The kurtosis value (1.93) suggests that the distribution of Repo Rate is mesokurtic, indicating a distribution close to normal. The average Reverse Repo Rate for public sector banks is approximately 5.14%. The average SLR for public sector banks is approximately 20.06%. The median SLR is close to the mean, indicating a roughly symmetric distribution. The maximum SLR observed is 23.00%. The minimum SLR observed is 18.15%.SLR has a moderate standard deviation of approximately 1.70, indicating moderate variability around the mean. SLR distribution is slightly right-skewed (0.31). The kurtosis value (1.72) suggests that the distribution of SLR is mesokurtic.

Table 4.4: Descriptive Statistics: Private Sector Banks:

| STATISTISTICS | CASA RATIO | CRR | NET INTEREST MARGIN | REPO RATE | REVERSE REPO RATE | SLR |

| Mean | 46.73967 | 3.975 | 3.547 | 6.035 | 5.145 | 20.06 |

| Median | 45.825 | 4.1 | 3.69 | 6.175 | 5.7 | 19.875 |

| Maximum | 60.68 | 4.5 | 4.39 | 8 | 6.25 | 23 |

| Minimum | 31.87 | 3.25 | 2.61 | 4 | 3.45 | 18.15 |

| Std. Dev. | 6.22107 | 0.38344 | 0.463444 | 1.335274 | 1.086306 | 1.69794 |

| Skewness | 0.197855 | - 0.6194 | -0.495484 | - 0.235549 | -0.629255 | 0.31217 |

| Kurto sis | 3.622135 | 2.175783 | 2.325521 | 1.925738 | 1.701627 | 1.72302 |

Source. EViews

The average CASA Ratio for private sector banks is approximately 46.74%, indicating that around 46.74% of their total deposits come from Current Account and Savings Account deposits.The median CASA Ratio is slightly lower than the mean, suggesting a slightly right-skewed distribution.The maximum CASA Ratio observed is 60.68%, indicating that some banks have a relatively high proportion of CASA deposits.The minimum CASA Ratio observed is 31.87%, indicating that some banks have a lower proportion of CASA deposits. CASA Ratio has a standard deviation of approximately 6.22, indicating moderate variability around the mean.The CASA Ratio distribution is slightly right-skewed (0.20), suggesting a slight tail to the right. The kurtosis value (3.62) suggests that the distribution of CASA Ratio is leptokurtic, meaning it has heavier tails and sharper peaks compared to a normal distribution. The average Net Interest Margin for private sector banks is approximately 3.55%. The median Net Interest Margin is slightly lower than the mean, suggesting a slightly left- skewed distribution. The maximum Net Interest Margin observed is 4.39%. The minimum Net Interest Margin observed is 2.61%. Net Interest Margin has a standard deviation of approximately 0.46, indicating moderate variability around the mean. The Net Interest Margin distribution is slightly left-skewed (-0.50). The kurtosis value (2.33) suggests that the distribution of Net Interest Margin is platykurtic.

Note: The independent variables which are the monetary variables are same for both public and private so descriptive interpretation given only once.

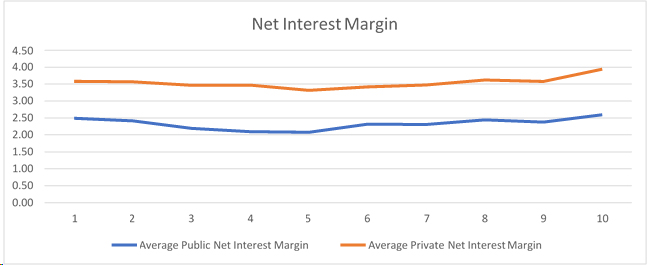

Fig 4.1 Net Interest Margin Line graph of Public and Private Sector Banks over the last 10 years

Source. Excel

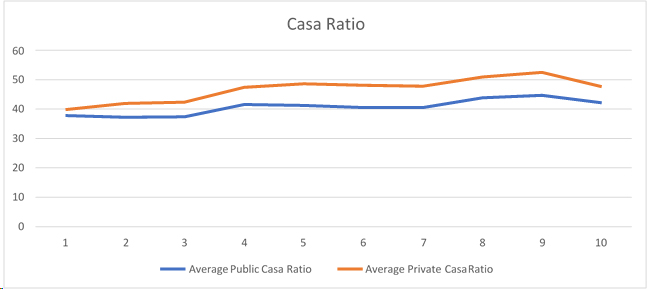

Fig 4.2 Casa Ratio Line graph of Public and Private Sector Banks over the last 10 years

Table 4.5: Correlation Matrix: Public Sector Banks:

| STATISTIC | CASA RATIO | CRR | NET INTEREST MARGIN | REPO RATE | REVERSE REPO RATE | SLR |

| CASA RATIO | 1 | - | - | - | - | - |

| CRR | -0.629 | 1 | - | - | - | - |

| NET INTEREST MARGIN | -0.124 | - 0.208 | 1 | - | - | - |

| REPO RATE | -0.653 | 0.698 | 0.236 | 1 | - | - |

| REVERSE REPO RATE | -0.329 | 0.574 | -0.039 | 0.79 | 1 | - |

| SLR | 0.116 | - 0.444 | 0.295 | -0.319 | -0.368 | 1 |

Source. EViews

The CASA ratio is a measure of a bank's deposits in current and savings accounts compared to total deposits. It has a negative correlation with CRR (-0.629), Repo Rate (-0.653), Reverse Repo Rate (-0.329), and SLR (0.116). This suggests that as the CASA ratio increases, CRR, Repo Rate, and Reverse Repo Rate tend to decrease, while SLR tends to increase, although the correlations are relatively weakThe Reverse Repo Rate is the rate at which the central bank borrows money from commercial banks. It has positive correlations with Repo Rate (0.79) and weak negative correlations with CASA Ratio (-0.329) and SLR (-0.368). SLR is the percentage of deposits that banks need to maintain in the form of cash, gold reserves, or other approved securities.

Table 4.6: Correlation Matrix: Private Sector Banks:

| STATISTIC | CASA RATIO | CRR | NET INTEREST MARGIN | REPO RATE | REVERSE REPO RATE | SLR |

| CASA RATIO | 1 | |||||

| CRR | -0.411 | 1 | ||||

| NET INTEREST MARGIN | -0.414 | -0.011 | 1 | |||

| REPO RATE | -0.48 | 0.698 | 0.229 | 1 | ||

| REVERSE REPO RATE | -0.23 | 0.574 | -0.003 | 0.79 | 1 | |

| SLR | -0.01 | -0.444 | 0.344 | -0.319 | -0.368 | 1 |

Source. EViews

The Repo Rate is the rate at which the central bank lends money to commercial banks. It has a positive correlation with CRR (0.698), Net Interest Margin (0.229), and Reverse Repo Rate (0.79). The Reverse Repo Rate is the rate at which the central bank borrows money from commercial banks. It has positive correlations with Repo Rate (0.79) and weak negative correlations with CASA Ratio (-0.23) and SLR (-0.368). SLR is the percentage of deposits that banks need to maintain in the form of cash, gold reserves, or other approved securities. It has a weak positive correlation with Net Interest Margin (0.344).

Table 4.7: Regression Analysis: Public Sector Banks: Casa Ratio

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.456 | 0.518 | 0.88 | 0.3883 |

| SLR | -0.609 | 0.642 | -0.949 | 0.352 |

| CRR | -2.06 | 0.967 | -2.13 | 0.0446 |

| Repo Rate | -2.24 | 0.723 | -3.099 | 0.0052 |

| Reverse Repo Rate | 2.02 | 0.943 | 2.14 | 2.14 |

| R-squared | 0.603 | Mean dependent var | 0.636 | |

| Adjusted R-squared | 0.531 | S.D. dependent var | 2.274 | |

| S.E. of regression | 1.557 | Akaike info criterion | 3.889 | |

| Sum squared resid | 53.381 | Schwarz criterion | 4.129 | |

| Log likelihood | -47.513 | Hannan-Quinn criter. | 3.961 | |

| F-statistic | 8.364 | Durbin-Watson stat | 2.166 | |

| Prob(F-statistic) | 0.000292 |

Source. EViews

The intercept term represents the value of the dependent variable (Casa Ratio) when all independent variables (SLR, CRR, Repo Rate, Reverse Repo Rate) are zero. In this case, it is 0.456, but it is not statistically significant (p-value > 0.05). A one-unit increase in SLR is associated with a decrease of 0.609 units in the Casa Ratio, holding other variables constant. However, this coefficient is not statistically significant (p-value > 0.05). A one-unit increase in CRR is associated with a decrease of 2.06 units in the Casa Ratio, holding other variables constant. This coefficient is statistically significant at the 5% level (p-value = 0.0446), indicating that changes in CRR have a significant impact on the Casa Ratio. 0.636. to 2 suggests no autocorrelation. Overall, the regression analysis suggests that the Casa Ratio of public sector banks is significantly influenced by variables such as CRR, Repo Rate, and Reverse Repo Rate. The model explains approximately 60.3% of the variability in the Casa Ratio, and it is statistically significant overall.

Table 4.8: Regression Analysis: Public Sector Banks: Net Interest Margin

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.105456 | 0.050704 | 2.079841 | 0.0494 |

| DCRR | -0.257309 | 0.094647 | -2.718623 | 0.0125 |

| DSLR | 0.069196 | 0.06285 | 1.10098 | 0.2828 |

| DREPO RATE | 0.275211 | 0.070766 | 3.88905 | 0.0008 |

| DREVERSE REPO RATE | -0.181268 | 0.092363 | -1.962553 | 0.0625 |

| R-squared | 0.474026 | Mean dependent var | 0.011852 | |

| Adjusted R-squared | 0.378394 | S.D. dependent var | 0.193332 | |

| S.E. of regression | 0.152427 | Akaike info criterion | -0.758691 | |

| Sum squared resid | 0.511145 | Schwarz criterion | -0.518721 | |

| Log likelihood | 15.24232 | Hannan-Quinn criter. | -0.687335 | |

| F-statistic | 4.95679 | Durbin-Watson stat | 1.722344 | |

| Prob (F-statistic) | 0.005297 |

Source. EViews

This coefficient is statistically significant at the 1% level (p-value = 0.0125), indicating that changes in CRR have a significant impact on the Net Interest Margin. The coefficient for DSLR is 0.069, but it is not statistically significant (p-value > 0.05), indicating that changes in SLR do not have a significant impact on the Net Interest Margin. This coefficient is statistically significant at the 0.1% level (p-value = 0.0008), indicating that changes in Repo Rate have a significant impact on the Net Interest Margin. The coefficient for DREVERSE_REPO_RATE is -0.181, but it is not statistically significant (p-value > 0.05), indicating that changes in Reverse Repo Rate do not have a significant impact on the Net Interest Margin. Overall, the regression analysis suggests that the Net Interest Margin of public sector banks is significantly influenced by changes in the Cash Reserve Ratio (CRR) and Repo Rate (DREPO_RATE). These variables collectively explain approximately 47.4% of the variability in the Net Interest Margin, and the regression model is statistically significant overall.

Table 4.9: Regression Analysis: Private Sector Banks: Casa Ratio

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.182588 | 1.051661 | 0.173619 | 0.8638 |

| DSLR | -1.3153 | 1.303582 | -1.00899 | 0.3239 |

| DCRR | -1.90575 | 1.963097 | -0.97079 | 0.3422 |

| DREPO RATE | -2.84693 | 1.467771 | -1.93963 | 0.0654 |

| DREVERSE REPO RATE | 2.228467 | 1.915737 | 1.163243 | 0.2572 |

| R-squared | 0.331041 | Mean dependent var | 0.868889 | |

| Adjusted R-squared | 0.209412 | S.D. dependent var | 3.55567 | |

| S.E. of regression | 3.161524 | Akaike info criterion | 5.305562 | |

| Sum squared resid | 219.8952 | Schwarz criterion | 5.545531 | |

| Log likelihood | -66.6251 | Hannan-Quinn criter. | 5.376917 | |

| F-statistic | 2.721729 | Durbin-Watson stat | 1.335285 | |

| Prob (F-statistic) | 0.055725 |

Source. EViews

The coefficient for DCRR is -1.906, but it is not statistically significant (p-value > 0.05), indicating that changes in CRR do not have a significant impact on the Casa Ratio for private sector banks. The coefficient for DREPO_RATE is -2.847, but it is marginally not statistically significant (p-value = 0.0654), indicating that changes in Repo Rate may have a potential but not significant impact on the Casa Ratio for private sector banks. The coefficient for DREVERSE_REPO_RATE is 2.228, but it is not statistically significant (p-value > 0.05), indicating that changes in Reverse Repo Rate do not have a significant impact on the Casa Ratio for private sector banks. Overall, the regression analysis suggests that the Casa Ratio of private sector banks may not be significantly influenced by the changes in Statutory Liquidity Ratio, Cash Reserve Ratio, Repo Rate, or Reverse Repo Rate. The model explains only about 33.1% of the variability in the Casa Ratio, and it may not be statistically significant overall.

Table 4.10: Regression Analysis: Private Sector Banks: Net Interest Margin

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.146916 | 0.066849 | 2.197739 | 0.0388 |

| DCRR | -0.04957 | 0.124784 | -0.39724 | 0.695 |

| DSLR | 0.16019 | 0.082862 | 1.933211 | 0.0662 |

| DREPO RATE | 0.194229 | 0.093299 | 2.081795 | 0.0492 |

| DREVERSE REPO RATE | -0.14103 | 0.121773 | -1.15815 | 0.2592 |

| R-squared | 0.294236 | Mean dependent var | 0.03963 | |

| Adjusted R-squared | 0.165916 | S.D. dependentvar | 0.220043 | |

| S.E. of regression | 0.200962 | Akaike info criterion | -0.20583 | |

| Sum squared resid | 0.888483 | Schwarz criterion | 0.034141 | |

| Log likelihood | 7.778692 | Hannan-Quinn criter | -0.13447 | |

| F-statistic | 2.292978 | Durbin-Watson stat | 1.530671 | |

| Prob (F-statistic) | 0.091679 |

Source. EViews

Overall, the regression analysis suggests that the Net Interest Margin of private sector banks may be significantly influenced by changes in the Repo Rate (DREPO_RATE) but not by changes in the Cash Reserve Ratio (DCRR) or Reverse Repo Rate (DREVERSE_REPO_RATE). The model explains only about 29.4% of the variability in the Net Interest Margin, and it may not be statistically significant overall.

5. Conclusion and suggestions

In conclusion, this research provides valuable insights into the impact of monetary policy on the profitability and liquidity of public and private sector banks in India. Through rigorous analysis encompassing unit root tests, descriptive statistics, correlation analysis, regression analysis, and Granger causality tests, several key findings have emerged. Firstly, both public and private sector banks exhibit stationarity in key variables, albeit with some variations in descriptive statistics and correlation patterns. Regression analysis reveals nuanced relationships between monetary policy variables and bank performance metrics, with differences observed between the sectors. Granger causality tests further highlight the complex interactions between monetary policy variables and bank indicators, underscoring the need for sector-specific considerations.

The findings suggest that while monetary policy exerts a significant influence on bank profitability and liquidity, the responses vary between public and private sector banks. These differences may stem from diverse business models, market positioning, regulatory environments, and sensitivities to policy changes. Therefore, future research should delve deeper into these sector-specific dynamics to enhance the understanding of monetary policy transmission mechanisms in the banking sector. Additionally, employing advanced econometric techniques and expanding the scope of analysis could provide more comprehensive insights into the heterogeneous impacts of monetary policy.

Overall, this research contributes to the existing literature by shedding light on the intricate relationship between monetary policy and bank performance in the Indian context.

Based on the comprehensive analysis conducted across unit root tests, descriptive statistics, correlation, regression, and Granger causality tests for both public and private sector banks, several key suggestions can be inferred to enhance the understanding of the impact of monetary policy on bank profitability and liquidity in India. Firstly, given the differences observed between public and private sector banks in their responses to monetary policy, future research endeavors should focus on deeper explorations of the underlying mechanisms driving these distinctions. This could involve qualitative studies delving into the organizational structures, governance frameworks, and regulatory environments of these banks to identify specific factors influencing their responses to policy changes.

Secondly, the findings from the regression analysis reveal significant relationships between monetary policy variables and key indicators of bank profitability and liquidity. Policymakers and regulators can leverage these insights to fine-tune monetary policy measures in a manner that supports the stability and resilience of the banking sector while promoting economic growth. For instance, a nuanced understanding of how changes in interest rates impact bank lending behavior can inform the calibration of policy tools to achieve desired credit growth targets. Furthermore, the Granger causality tests provide valuable insights into the direction and strength of causality between monetary policy variables and bank performance indicators. This information can guide policymakers in designing more effective policy interventions aimed at enhancing the transmission mechanism of monetary policy and ensuring its alignment with broader economic objectives. Additionally, the correlations identified between different monetary policy variables and bank performance metrics highlight the interconnected nature of these factors. Policymakers should adopt a holistic approach to monetary policy formulation, considering the simultaneous effects of multiple policy instruments on various aspects of bank operations, including lending behavior, interest rate spreads, and liquidity management. Moreover, the unit root tests confirm the stationarity of key variables, providing a robust foundation for further time-series analysis and modeling. Researchers can build upon these findings by employing advanced econometric techniques such as vector autoregression (VAR) or structural equation modeling (SEM) to unravel the dynamic interactions between monetary policy, bank behavior, and macroeconomic outcomes.

In conclusion, the findings from this research underscore the importance of continued empirical investigation into the nexus between monetary policy and bank performance. By leveraging insights from diverse analytical approaches, policymakers, regulators, and market participants can develop more informed strategies to promote financial stability, enhance the efficiency of monetary policy transmission, and support sustainable economic development.

REFERENCES

About Anubha Srivastava

Anubha Srivastava is a proven academician, keynote speaker, and corporate trainer with over 13 years of experience in India, Indonesia, and Africa. Currently a Consultant for PT. DJerapah Magah Plasindha and a Visiting Faculty at Universitas Diponegoro and UNNES in Indonesia, she has played pivotal roles in academic and training initiatives such as the Pan Africa e-network project. With an illustrious academic background from institutions like Harvard Business Schoolx and Amity University, she has shared her expertise with entities like TATA Motors, NTPC, and the Indian Army. Additionally, she has published over 28 research papers in reputable journals, served as an editor and peer reviewer for acclaimed publications, and been a keynote speaker at international conferences.

Disclaimer : The opinions expressed in this article are the personal opinions of the author. The facts and opinions appearing in the article do not reflect the views of Indiastat and Indiastat does not assume any responsibility or liability for the same.

Fix Execution Gaps, Not Policy: India’s Education Reality... Read more

.png)

.png)